Table of contents:

- Why Checkout Failures Matter for UK Retailers

- The Most Common Checkout Failure Points

- How Second Line & Retail Finance Reduce Checkout Drop-Off

- Building a Resilient Checkout

- FAQs

Why Checkout Failures Matter for UK Retailers

Checkout is the stage with the greatest commercial intent. When a customer reaches the checkout point, they have already researched, compared, and committed. Even the slightest bit of friction at this point can result in a lost sale.

According to the Baymard Institute:

“The average documented online shopping cart abandonment rate is 69.99%.”

For UK merchants operating in one of Europe’s biggest and most competitive e-commerce markets, that’s a lost intent with significant value. Consumers demand speed, flexibility, and choice when it comes to payment.

The problem isn’t just driving traffic. When a checkout fails, revenue is lost.

The Most Common Checkout Failure Points for UK Merchants

Payment Declines & False Declines

One of the most significant checkout failure points in the UK merchants face is payment decline both legitimate and false.

Common Causes:

- Insufficient funds

- Card expiry or incorrect details

- Fraud prevention filters

- Credit underwriting thresholds

For merchants offering finance, underwriting thresholds introduce another layer of risk. When a prime lender declines an application, many retailers treat that as the end of the journey.

But it doesn’t have to be.

The Second Line Opportunity

“Second line” or “second look” lending refers to customers declined by a prime lender being automatically referred to a secondary lender, with an alternative risk appetite.

Instead of losing the sale entirely:

- The customer receives a seamless alternative decision

- Approval rates increase

- Revenue recovery improves

Declined prime applications are often recoverable by structured second-line underwriting, especially for near-prime customers.

For UK merchants, structured lending tiers can assist in securing more approvals while still being compliant with the FCA regulated finance checkout requirements.

Lack of Flexible & Second Line Payment Options

If a shopper:

- Can’t pay upfront

- Fails a prime credit check

- Has a thin credit history

They often abandon.

The FCA Woolard Review highlighted the rapid growth of Buy Now Pay Later (BNPL), noting:

“BNPL products have become increasingly popular as an alternative to traditional credit.”

Consumer demand for flexible credit options in the UK continues to grow.

Without layered finance options:

- Approval rates drop unnecessarily

- Customer acquisition costs rise

- Merchants lose otherwise creditworthy customers

This is where second line lending solutions play a strategic role.

Rather than expanding risk blindly, merchants can implement:

- Prime lenders

- Structured second-line options

- Clear, compliant, affordability checks

This approach is particularly effective in higher AOV(average order value) sectors such as home improvements, dental, automotive and retail technology.

The second line isn’t just a risk tool, it’s a conversion recovery tool.

Mobile Checkout Friction

The majority of UK ecommerce transactions are mobile-first. Yet many finance journeys still feel desktop-built.

Common issues include:

- Long underwriting forms

- Excessive data entry

- Poor field validation

- Slow page loads

Finance apps that are not optimised for mobile materially reduce the finance conversion rates merchants could otherwise achieve.

When a customer fails to access prime credit on mobile and is required to manually restart the journey with a new provider, abandonment is almost inevitable.

Instead, the experience should be a seamless, automated referral not a rejection or a re-application.

Forced Account Creation

Baymard research consistently identifies forced account creation as a leading cause of checkout abandonment.

For finance journeys, this friction is amplified when:

- Customers must create user accounts before applying

- Duplicate data entry is required

- Forms are not pre-filled

Best practice for reducing friction:

- Offer guest checkout

- Clearly show progress indicators

- Offer auto-fill where possible

When the path feels simple and linear, drop-off reduces.

Hidden Fees & Transparency Issues

Trust is critical in finance checkout.

Under FCA Consumer Duty (PS22/9):

“Firms must deliver good outcomes for retail customers.”

UK merchants offering finance must ensure:

- Clear APR disclosure

- Transparent repayment terms

- No hidden fees

- Accurate representative examples

This becomes especially important when multiple lending tiers exist. If prime and second-line rates differ by risk profile, transparency must remain absolute.

Clear communication protects:

- Customer trust

- Brand reputation

- Regulatory compliance

Clear APR communication is especially critical where multiple lending tiers exist. When prime and second-line rates vary by risk profile, disclosures must remain transparent, consistent, and easy to understand.

Technical Failures & Speed

Even minor technical friction can create major revenue leakage.

Common issues include:

- Payment gateway API timeouts

- Finance decision delays

- Broken integrations

- Script conflicts

In finance checkout, speed matters. Customers expect near-instant decisions.

If second-line referral is not automated via API and requires excessive manual customer intervention, merchants risk:

- Customer confusion

- Lost trust

- Abandoned sessions

Technical reliability is not just operational, it’s commercial.

The Hidden Revenue Cost of Declined Applications

Many merchants underestimate how much revenue is lost through finance declines. In a scenario with 10,000 monthly checkouts, if 15% of customers apply for finance, that results in 1,500 applications.

With a 30% prime decline rate, 450 of those customers are declined, representing stalled revenue at the point of checkout. If 20% of those declined customers are recoverable through a second-line lender, that generates approximately 90 additional approvals. At an average order value of £1,200, this equates to £108,000 in incremental monthly revenue, or £1,296,000 annually.

Crucially, this revenue comes from customers already in the funnel, requires no additional marketing spend or increase in traffic, and is purely the result of improved conversion.

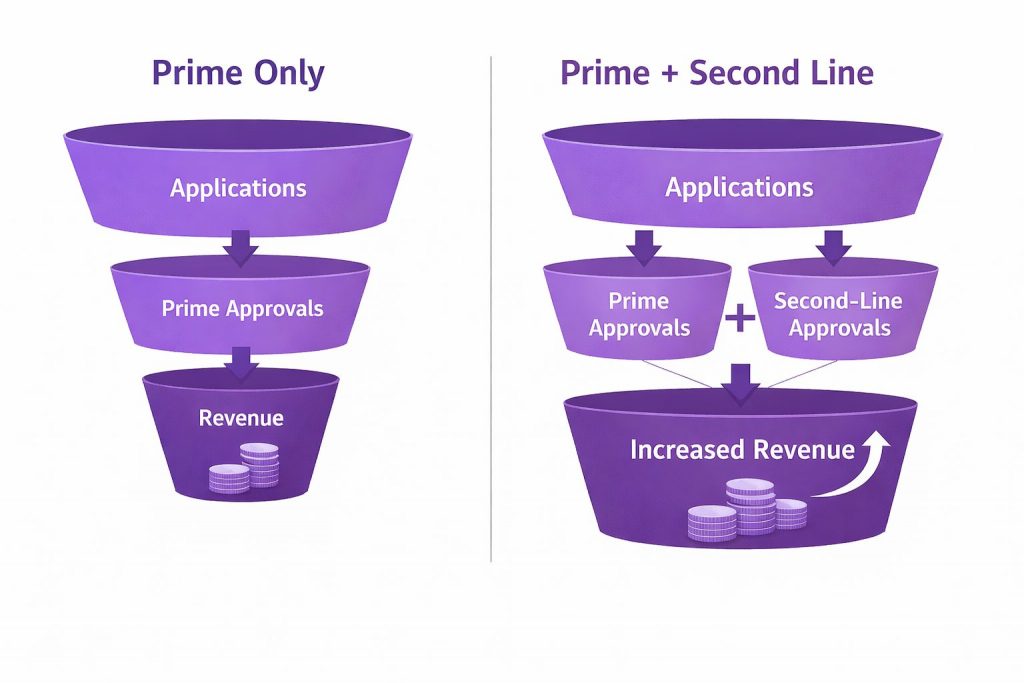

Funnel Comparison

Second line transforms declines from a dead end into a managed conversion extension.

How Second Line & Retail Finance Reduce Checkout Drop-Off

Checkout drop-off typically happens when willing customers don’t qualify for prime lending. By integrating second line and retail finance solutions, merchants can improve approval rates and acquire near-prime customers who would otherwise be declined.

This structured process ensures the customer experience remains seamless, further improving experience continuity and eliminating wasted traffic spend due to declined applications.

For UK merchants, Payl8r’s FCA-regulated retail finance solutions enable prime and second-line journeys without adding complexity to the operations, thus helping to increase conversions while upholding responsible lending practices.

Building a Resilient Checkout

A resilient checkout is built to win more customers, mitigate risk, and stay completely compliant with no extra friction.

Resilient Checkout Checklist:

- Multi-payment approach: Provide card, mobile payment, and retail finance options to give customers maximum choice and conversion.

- Clear credit transparency: Display clear, compliant credit information upfront to increase trust and FCA compliance.

- Automatic second-line referral: Refer near-prime customers smoothly to alternative finance options.

- Mobile-first finance UX: Ensure finance applications are optimised for fast, seamless mobile completion.

- Consumer Duty alignment: Align fair value, clarity, and good customer outcomes throughout the customer journey.

A resilient checkout isn’t just about reducing abandonment, it’s about protecting revenue at the moment of highest intent.

FAQ‘s

Payment declines, lack of flexible finance options, mobile friction, forced account creation, hidden fees and technical integration failures are among the most common checkout issues affecting UK ecommerce businesses.

Common reasons include insufficient funds, expired cards, fraud filters, incorrect details and Strong Customer Authentication (SCA) challenges under PSD2 regulations.

With average abandonment rates near 70%, even small improvements in approval rates or friction reduction can translate into significant incremental revenue particularly for higher AOV sectors

Payment friction and lack of suitable payment options consistently rank among the leading causes. When customers cannot complete payment in their preferred way, they leave.

By optimising mobile UX, reducing unnecessary form friction, implementing automated second-line finance and ensuring regulatory transparency.

Yes. Offering structured, regulated finance checkout options including second line lending can improve approval rates and reduce abandonment, particularly for higher-value purchases.